ICON BRICKELL, a three-tower complex

in Miami’s financial district, was supposed to be a flagship project for the

Related Group, the city’s top condominium developer. It would boast 1,646

luxury condos, a 91-metre-long pool, and a hundred 22-foot columns in its

entryway. By 2010, however, it had become a symbol of the excesses of the

city’s building boom, and Related was forced to hand two of the towers to its

banks. Miami condo prices plunged to 60% below their peak. The vacancy rate

jumped to 60%. Predictions flew that the market, the epicentre of America’s

property crash, would take ten years to come back, or even longer.

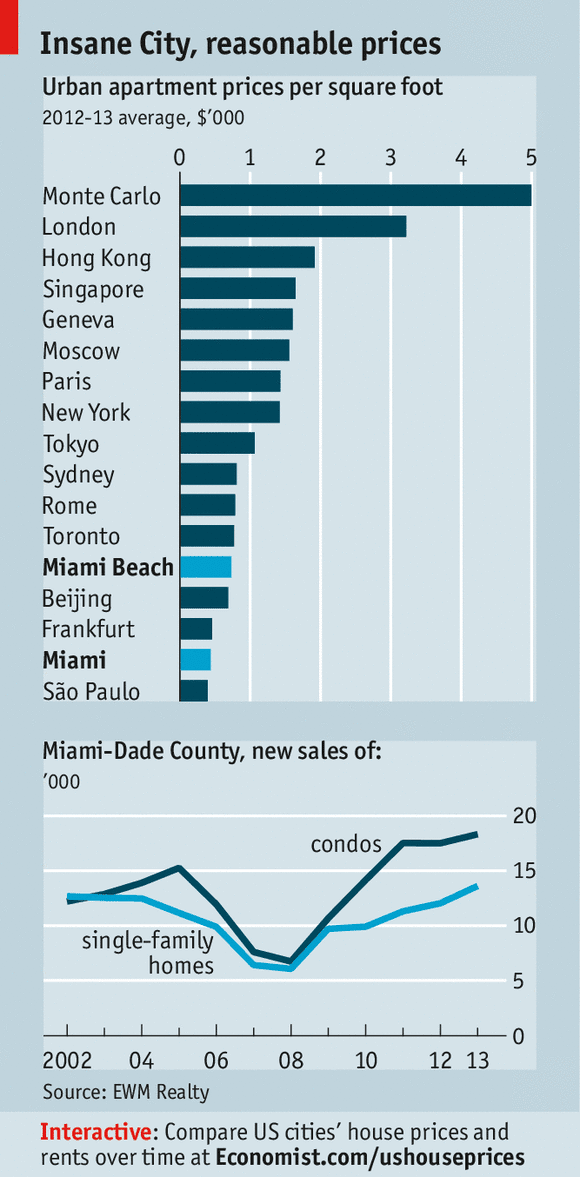

The speed of the recovery has

surprised everyone. Condo prices are already back near peak levels in Miami’s

most desirable areas, and at 75-80% elsewhere. The available supply of units

has fallen back to within the six-to-nine-months-of-sales range considered

normal, from a stomach-churning 40 in 2008. Only 3% of condos are unoccupied.

Sales of condos and single-family homes are above pre-crisis levels across

Miami-Dade County. Commercial property, too, has rebounded, with demand

outstripping supply. Developers are once again relaxed enough to crack jokes.

“I call the current expansion the Viagra cycle,” jokes Carlos Rosso, Related’s

president of condominium development. “We just want it to last a little

longer.”

The recovery has been partly driven

by low interest rates and bottom-fishing by private equity, which helped to

clear excess inventory. But the biggest factor is that the city nicknamed the

“Capital of Latin America” has attracted a flood of capital from Latin America.

Rich people in turbulent spots such as Venezuela and Argentina are seeking a

safe haven for their savings.

Estate agents are also seeing

capital flight from within the United States. Individuals pay no state or city

income tax in Miami, unlike, say, New York, whose mayor wants to hike taxes on

the rich further. “Somebody said to me, ‘Give me three reasons why this will

continue.’ My answer was: Maduro, Kirchner and De Blasio,” chuckles Marc

Sarnoff, a Miami city commissioner, referring to the leaders of the

capitalist-bashing regimes in Venezuela, Argentina and New York.

Another attraction is the 40% rise

in Miami condo rents since 2009, buoying the income of owners who choose not to

live in the tropical hurly-burly that Dave Barry, a local author, calls “Insane

City”. Brokers report increased business from Eastern Europe and the Middle

East (Qatar Airways will fly direct to Miami from June), and an uptick in

inquiries from Chinese buyers.

Is another bubble forming already?

Developers say this time is different, and in some ways it is. In a few years

Miami has gone from the most- to the least-leveraged property market in

America. Buyers of new condos typically have to put 50% down, half of that

before building starts. Banks are loth to extend construction loans unless

60-75% of the units are already sold. In both residential and commercial

projects, they require developers to put in much more equity than before. Mr

Rosso says Related now puts in three times as much, which limits its ambition.

The firm now has 2,000 condos in the works, a tenth of what it was building in

2007.

Is another bubble forming already?

Developers say this time is different, and in some ways it is. In a few years

Miami has gone from the most- to the least-leveraged property market in

America. Buyers of new condos typically have to put 50% down, half of that

before building starts. Banks are loth to extend construction loans unless

60-75% of the units are already sold. In both residential and commercial

projects, they require developers to put in much more equity than before. Mr

Rosso says Related now puts in three times as much, which limits its ambition.

The firm now has 2,000 condos in the works, a tenth of what it was building in

2007.

Still, a supply glut is possible.

With developers gung-ho again, around 50 towers are under construction or

planned in downtown Miami (including the Porsche Design Tower, whose

well-heeled inhabitants will be able to take their cars up to the level on

which they live in a special lift—this is useful if you really love your car).

More were added last month when Oleg Baybakov, a Russian mining-to-property

oligarch, bought a trio of condo-development sites for $30m, more than triple

their assessed market value in 2013.

Miami’s developers are adept at

using “smoke and mirrors” to hide the true number of pre-sold units, says Peter

Zalewski of Condo Vultures, a property-intelligence firm. Some see the first

signs of trouble. The stock of unsold condos and houses has crept up slightly

since last summer. A local broker says that Blackstone, a private-equity firm

with a taste for bricks and mortar, bought $120m of properties with his firm’s

help in 2013 but “won’t do anything like that this year”. Mr Zalewski says

banks are competing harder to finance certain projects, but this may not be a

sign of unadulterated bullishness. They may simply be betting that many of the

134 towers proposed but not yet under construction in South Florida won’t get

built—meaning the 57 that have already broken ground will do better than

forecast.

Much will depend on whether Latin

Americans remain addicted to Miami property and, should their ardour cool, whether

Americans and others would take up the slack. Few domestic buyers are

comfortable putting 50% down, especially when most of it is at risk if the

project fails. One or two developers have begun to accept 30% down, a possible

sign of increased reliance on home-grown buyers.

The market should get a fillip from

the current and planned redevelopment of several chunks of downtown Miami. One

of the most ambitious projects is Miami Worldcenter, a 30-acre retail, hotel

and convention-centre complex that will feature Bloomingdale’s, Macy’s and a

giant Marriott hotel. A science museum will soon join the art museum.

No comments:

Post a Comment

Per favore lasciate il vostro commento o domanda qui: